NEWS &VIEWS

Forecasts, Commentary & Analysis on the Economy and Precious Metals

Celebrating our 46th year in the gold business

May 2020

“The reality is the world will never be the same after the coronavirus.” – Henry Kissinger

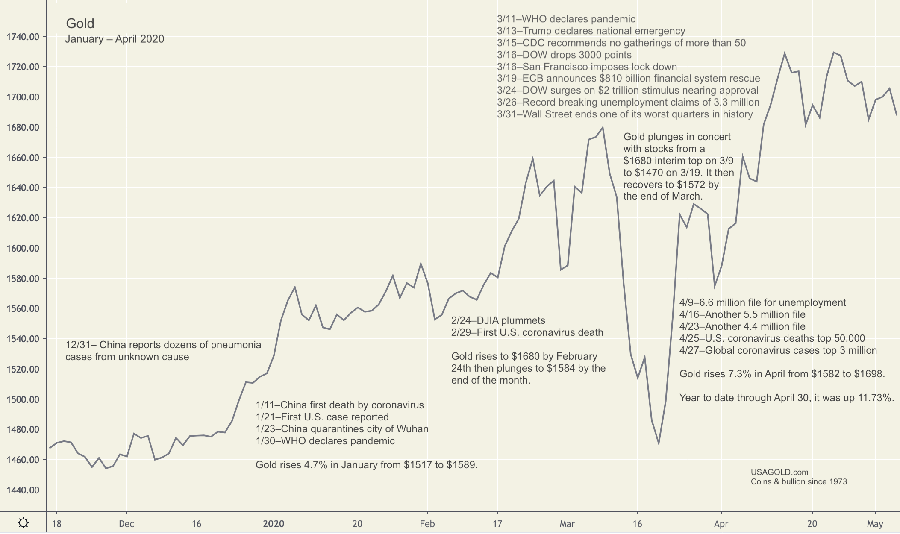

Gold in the year of the pandemic

What it cannot do is cure the virus. What it could do, however, according to a good many analysts, is act as an effective hedge against its economic consequences. Since the beginning of the year through April, the metal was up 11.73% during probably the worst period in economic history since the 1930s Great Depression. Below we chronicle what top experts have to say about gold in the year of the pandemic – its portfolio role, its qualities as a disaster hedge, and its price potential.

Sources: TradingView.com, NBC News

Click to enlarge

Hedge fund involvement in gold deep and unlikely to unwind soon

Financial Times ran a comprehensive report on recent involvement of hedge funds in the gold market citing several prominent names, among them Paul Singer’s Elliot Management. “New York-based Elliott,” says FT, “which manages about $40bn in assets, told its investors last month that gold was ‘one of the most undervalued’ assets available and that its fair value was ‘multiples of its current price’.” Hedge funds have been among the chief supporters of the gold bullion market in recent months. Gold ETFs, the primary beneficiary of that interest, added a strong 298 tonnes to their holdings in the first quarter of the year, according to the World Gold Council. Total ETF holdings now stand at 3,185 tonnes – a new record and the third-largest holding after the United States (8,133.5 tonnes) and Germany (3,373.6 tonnes).

Hedge fund involvement in the gold market is deep, the players are prominent, and their commitments, given the rationales publicly stated, are unlikely to unwind anytime soon. “ALL the smart money,” writes market analyst Fred Hickey at his Twitter feed, “Dalio, Druckenmiller, Tudor Jones, Zell, Gundlach, Singer, Klarman, Einhorn, Mobius (and some who I know are loading up but are doing it quietly) are long gold and understand the simple concept Hugh Hendry explains here. Question is: What are YOU waiting for?” Hickey then reposts famed hedge fund manager Hugh Hendry’s comments: “Today, however, ‘if you fear inflation then you should buy more gold.’ It is simple. The Fed is trying to debase the $ to help the economy. Will it help? Maybe. Will it help the stock market? Probably. Will it help gold? Definitely. This is the final leg that I envisaged in 2002.”

Bank of America says gold is going to $3000

“[B]eyond traditional gold supply and demand fundamentals,” writes Bank of America in a client memo referenced at Barron’s and titled The Fed Can’t Print Gold, “financial repression is back on an extraordinary scale. … Beyond real rates, variables such as nominal GDP, central bank balance sheets, or official gold reserves will remain the key determinants of gold prices, in our view. As central banks and governments double their balance sheets and fiscal deficits respectively, we have also decided to up our 18 month gold target from $2,000 to $3,000/oz.”

Jim Rogers, Steve Forbes jump on the gold bandwagon

Popular commentator Jim Rogers from Beeland Interests has not publicly recommended gold for quite some time, but now that has changed. He told Financial Times that he started buying gold last year and that “inflows into gold and silver will increase as investors lose confidence in government money-printing experiments.”

Steve Forbes also jumped on the gold bandwagon recently saying “the trillions of dollars being spent to save our virus-battered economy are stoking fears of inflation. Gold has always been a hedge against government’s economic blunders.” Forbes’ declaration of interest in gold though does not come as a great surprise. At one time, he advocated a gold standard for the United States as the best way to restore a sound dollar.

Bloomberg’s John Authers enlists his considerable analytical skills to explain what gold might be telling us about the economy and the stock market. “A rising gold price,” he says in a recent column headlined “Gold still shines 50-years after Nixon. Will Netflix?“, “is always a disquieting sign … The stock market, home of optimists everywhere, is doing very well at present. But gold, where pessimists find a home, is doing even better. In dollars, the shiny metal closed on Tuesday at its highest since 2012. The all-time high is in sight, and it has gained more than 60% since its nadir in 2015.”

Over the past twelve months through Friday, May 8, gold is up 33.4%. It is up 11.73% year to date through April. The Dow Jones Industrial Average is down 6.7% over the past twelve months – and 16.1% year to date.

Cartoon courtesy of MichaelPRamirez.com

Cartoon courtesy of MichaelPRamirez.com

Inflation or deflation? Gold doesn’t care

There are two schools of thought on where we could end up ultimately the result of the aggressive measures deployed monetarily and fiscally by governments and central banks. One says the stimulus fails and we end up in a deflationary depression. The other says it works and we end up with runaway inflation, perhaps even hyperinflation. Some, more optimistic analysts see “V”, “U” and “W” shaped recoveries in our economic future. The worry, though, is that even if such a recovery were to occur, it would be flawed and serve as a precursor to a less than desirable outcome.

Physical gold ownership – and we emphasize the word physical as in the form of coins and bullion – is a peace of mind investment. It balances error elsewhere in your portfolio structure and takes the emphasis off deciding on inflation or deflation simply because it protects, as analyst Clif Droke points out in his regular Seeking Alpha column, against either eventuality. Historically, it is the ultimate store of value and safe haven simply because it is an asset that is not simultaneously someone else’s liability.

“Historically, investors turn to gold at both extremes of the long-term economic cycle; those two extremities encompass both inflation and deflation. Although many consider gold as being mainly an inflation hedge, a historical overview of the metal’s performance shows that gold tends to benefit just as much from the threat of deflation than from inflation. The proof of this can be seen by gold’s outstanding performance during 2008-2011, and again in 2018-2020 when deflationary undercurrents were sweeping some of the world’s biggest economies.

But gold also clearly has benefited when inflation becomes a problem for the U.S. economy in particular. The last time gold was driven by inflation concerns was during the years between 2002 and 2007 when commodity prices were booming as wartime spending was massive, and the U.S. dollar was rapidly losing value.”

Continued below ………

If you think you could benefit from a concise review of the latest news, analysis, and opinion on the gold market from a variety of expert sources, then News & Views is the newsletter for you. Since the early 1990s, we have offered it free-of-charge as a monthly service to our regular clientele and as an incentive to prospective clients without obligation. By subscribing, you will automatically receive future editions and occasional in-depth Special Reports by e-mail.

If you think you could benefit from a concise review of the latest news, analysis, and opinion on the gold market from a variety of expert sources, then News & Views is the newsletter for you. Since the early 1990s, we have offered it free-of-charge as a monthly service to our regular clientele and as an incentive to prospective clients without obligation. By subscribing, you will automatically receive future editions and occasional in-depth Special Reports by e-mail.