NEWS &VIEWS

Forecasts, Commentary & Analysis on the Economy and Precious Metals

Celebrating our 46th year in the gold business

FEBRUARY 2020

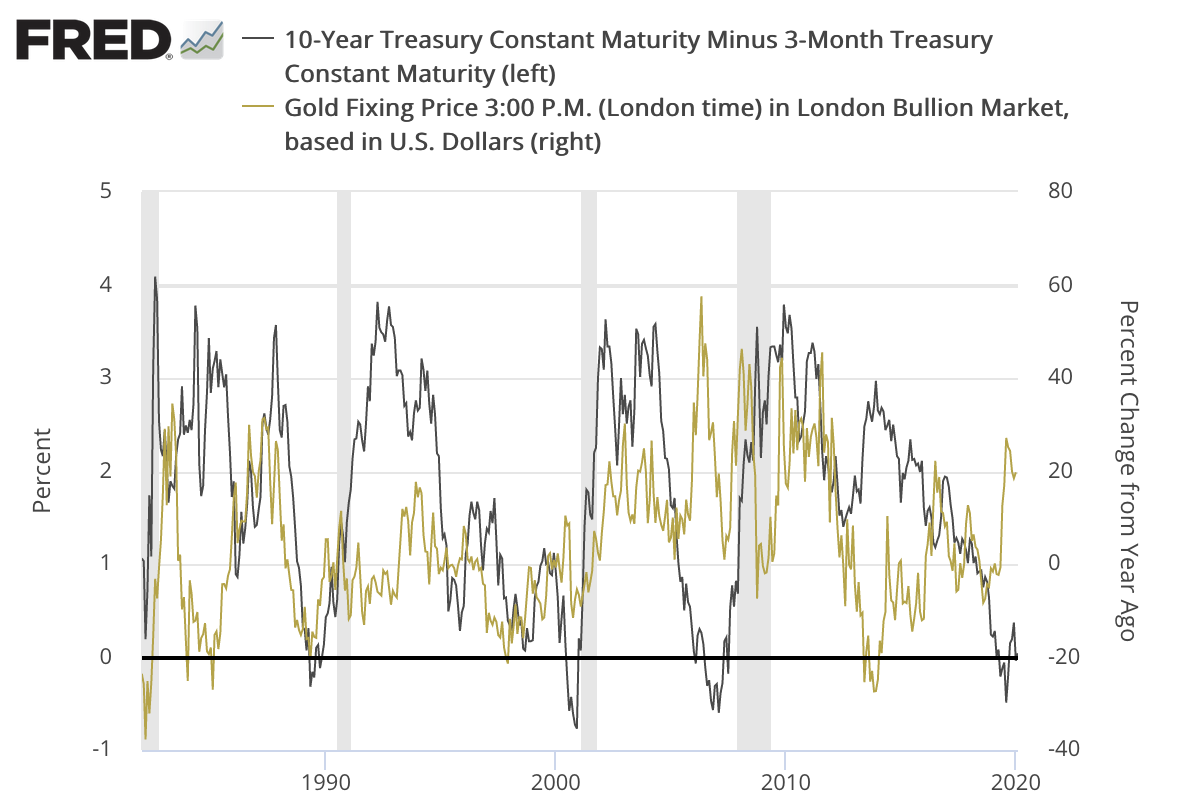

Yield inversions as a harbinger of recessions and higher gold prices

During the course of the past several months, we have heard much about the inverted yield curve in three-month and ten-year Treasuries as a harbinger of recessions. Missed in the press reports is the fact that it has also been a harbinger of higher gold prices. In the chart above, please note the upward surges in the price of gold following the three most recent yield inversions in 1989, 2000 and 2006. Those price rallies, it is now well understood, came in response to aggressive central bank stimulus intended to beat back the ill effects of the recessions that followed in 1990, 2001 and 2008.

In recent months, as shown in the chart, the yield differential between the ten-year and three-month Treasury yield has again pinched to zero. After briefly recovering at the end of the year, it dropped to the zero line again a few weeks ago. Note, as well, the sudden rise in the price of gold from the time the inversion first made its appearance in May of last year – a more than 20% increase.

Source: St. Louis Federal Reserve [FRED]

Source: St. Louis Federal Reserve [FRED]

Chart note: The grey bars indicate recessions.

Are the markets hooked on Fed stimulus?

Fed Chairman Jerome Powell’s forceful statement that the Fed is “determined” to avoid a disinflationary outcome in the United States is a clear indication of the central bank’s intentions. The question hanging over the markets is whether or not the central bank’s policies will deliver the intended result. At the same time, it seems the Fed is not only reluctant to back down from the dovish course of action already in place, but it could also be intent in upping the ante by providing the necessary “liquidity” as long as credit markets need it – no matter how the policy is labeled.

“In essence,” says analyst Jim Bianco in a Bloomberg opinion piece, “the Fed has become the lender of first resort when it should be the lender of last resort and offer repo at a penalty rate. The Fed should be willing to help a dealer in need, but it should come at a price.” Some of the more skeptical on Wall Street are asking “what happens when QE4 is turned off?” The better question might be “what happens if it is not?”

Why financial advisers should line their portfolios with gold

More and more, it is becoming a mainstay in the financial business that the wise investor and/or financial advisor embrace gold as a means to capital preservation in a rapidly changing and increasingly dangerous investment climate. In Cazenove Capital’s case, it is emphasizing gold as a hedge against geopolitical turbulence. “Speaking at a Schroders breakfast briefing yesterday (January 22),” reports Financial Times, “Janet Mui, global economist at Cazenove Capital, said she thought investing in gold was the best way for advisers and fund managers to hedge the risks in their portfolios. She said: ‘Gold has the feature of portfolio hedging and diversification. Gold should be in your portfolio.’”

Related, please see:

Precious metals for financial planners and advisors

We will work with you to offer your clients a strong, service-based

presence in the gold coin and bullion market

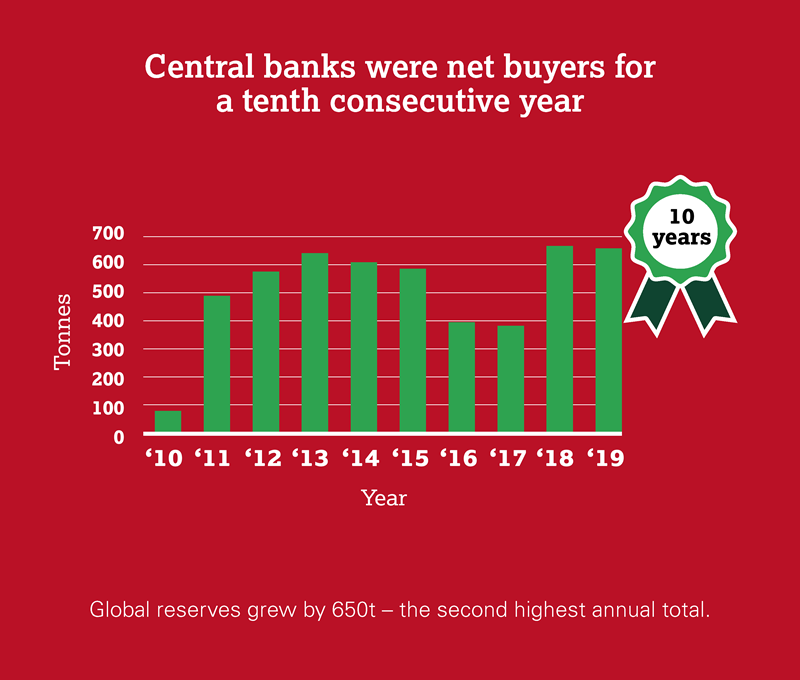

Central bank gold demand for 2019 second-highest level in 50 years

“Gold demand,” says the World Gold Council in its Demand Trends analysis for the year 2019, “fell 1% in 2019 as a huge rise in investment flows into ETFs and similar products was matched by the price-driven slump in consumer demand. . . Central bank demand also slowed in the second half – down 38% in contrast with H1’s 65% increase. But this was partly due to the sheer scale of buying in the preceding few quarters and annual purchases nevertheless reached a remarkable 650.3t – the second-highest level for 50 years.”

We are quite a distance from the days when central banks were net sellers of gold. Some central banks are building reserves. Others are making certain that gold is repatriated within their borders. Few are selling and when they do it is usually under stressed circumstances. De Nederlandsche Bank, the Dutch central bank, recently offered a bedrock reason for the official sector’s interest in building and maintaining gold reserves. “[I]f the system collapses,” it said, “the gold stock can serve as a basis to build it up again. Gold bolsters confidence in the stability of the central bank’s balance sheet and creates a sense of security.’”

In the same week the World Gold Council released its analysis, GFMS published its annual assessment of gold market fundamentals and price outlook. “While demand from key Asian markets will likely to remain weak this year,” it advises, “ongoing central bank purchases and renewed investor interest will lend support for higher gold prices. We therefore expect gold to average $1,558/oz in 2020, with a possibility to test and move beyond $1,700/oz later in the year.”

(Please see GFMS Research/Review and Outlook/January 2020)

Image courtesy of the World Gold Council

Image courtesy of the World Gold Council

The best-performing asset of the 21st Century

Echoing a theme, we advanced in this newsletter several months ago, Charlie Morris of Atlantic House Fund Management in the United Kingdom says “Gold remains the best-performing mainstream asset of the 21st century, yet investors own a mere 82 million ounces (worth $128bn) between them via the exchange-traded funds. That might sound like a substantial holding, but it is not. With global exchange-traded funds worth over $5trn, the implication is that the average portfolio has a mere 2% allocation to gold. Academic studies range in their conclusions, but they all suggest the optimized allocation should be greater than zero. I have often felt that 8% makes sense for a balanced portfolio and 15% to 25% for an all-weather total return fund.”

The question becomes whether or not an investment that has performed so well in the past is likely to perform equally well in the future. Though nothing in the world of finance and economics is certain, we rest the bullish case for gold on the understanding that none of the economic and financial system problems that created a positive price environment for gold over the last nearly nineteen years have been removed from consideration. In fact, a case could be made that they have only intensified – and dangerously so. Gold is up 5% through January of the new year while the Dow Jones Industrial Average dropped 1%.

Please see: Gold’s Century: While stocks dominated headlines, gold quietly performed

If you think you could benefit from a concise review of the latest news, analysis and opinion on the gold market from a variety of expert sources, then News & Views is the newsletter for you. Since the early 1990s, we have offered it free-of-charge as a monthly service to our regular clientele and as an incentive to prospective clients. By subscribing, you will automatically receive future editions and occasional in-depth Special Reports by e-mail.

If you think you could benefit from a concise review of the latest news, analysis and opinion on the gold market from a variety of expert sources, then News & Views is the newsletter for you. Since the early 1990s, we have offered it free-of-charge as a monthly service to our regular clientele and as an incentive to prospective clients. By subscribing, you will automatically receive future editions and occasional in-depth Special Reports by e-mail.