NEWS &VIEWS

Forecasts, Commentary & Analysis on the Economy and Precious Metals

Celebrating our 46th year in the gold business

May 2019

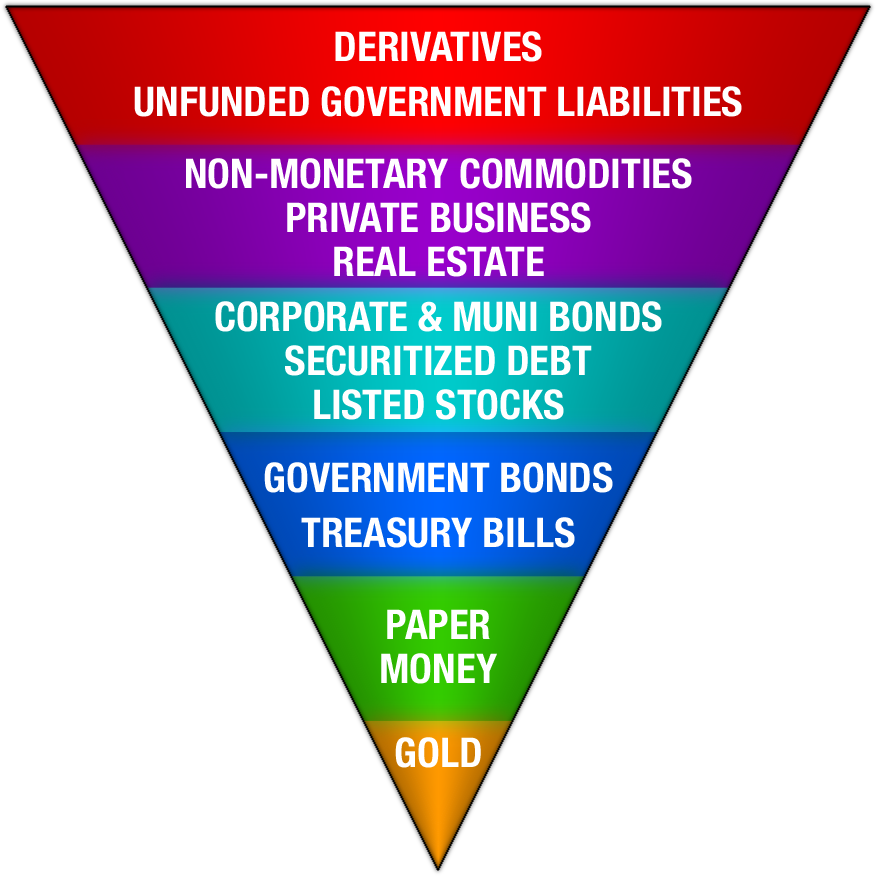

The Exter Inverted Pyramid of Global Liquidity

Credit risk, liquidity and gold

In a recent edition of Credit Bubble Bulletin, Doug Noland, the long-time critic of contemporary monetary policy, writes about the odd times in which we live from a financial perspective. “Such a precarious time in history,” he laments. “So much crazy talk has drowned out the reasonable. Deficits don’t matter, so why not a trillion or two for infrastructure? Our federal government posted a $691 billion deficit through the first six months of the fiscal year – running 15% above the year-ago level. Yet no amount of supply will ever impact Treasury prices – period. A Federal Reserve governor nominee taking a shot at ‘growth phobiacs’ within the Fed’s ‘temple of secrecy’, while saying growth can easily reach 3 to 4% (5% might be a ‘stretch’). Larry Kudlow saying the Fed might not raise rates again during his lifetime. Little wonder highly speculative global markets have become obsessed with the plausible.”

In that essay, Noland goes on to note having been influenced by the highly regarded Dr. Kurt Richebacher (1918-2007). Although he actually worked directly with the Austrian economist/banker, my connection came only as an appreciative reader of the Richebacher Letter (in pre-internet times) and his Wall Street Journal editorials. Richebacher concerned himself regularly with the interplay between financial market credit leverage, ordinary investors and the real economy. Please see International Precious Metals & Commodities Fair – Munich, Germany Transcript of Dr. Kurt Richebächer’s Lecture (USAGOLD, November 19, 2005). In re-reading that lecture, I am struck with how much of Richebacher’s analysis at the time can be applied to the present and a very similar set of circumstances. Now that Noland has acknowledged Richebacher’s influence, it explains to a large degree why his writings – like the snippet above – strike a chord with those of us concerned with the financialization of the markets.

In this context, we reproduce at the top John Exter’s famed Inverted Pyramid of Global Liquidity. Exter, who was an economist at the Federal Reserve and highly-respected analyst, made a fortune by purchasing gold just before Richard Nixon’s devaluation of the dollar in 1971 and its rapid ascent in the ensuing decade.

“His pyramid,” explains Capital Wealth Advisor’s Lewis Johnson, “stands upon its apex of gold, which has no counter-party risk nor credit risk and is very liquid. As you work higher into the pyramid, the assets get progressively less creditworthy and less liquid. For instance, paper money here means cash, which is recognized everywhere but is ultimately dependent upon the creditworthiness of the U.S. government. Farther up the pyramid, we find longer-dated U.S. government debt, which like cash is dependent upon the full faith and credit of the U.S. government – but on a longer time horizon. The next level is debt of municipals and corporations, whose value is more safely assured than that of more junior claims, such as investments in stocks, the junior tranche of a corporation’s capital structure. A rough estimate of the global liquid financial markets would place their value close to $100 trillion. This number grows further still as less liquid assets are added, such as private businesses, real estate and ultimately bank derivatives, the largest and murkiest of all assets.”

In a credit crisis, he concludes, “this bloated structure pancakes back down upon itself in a flight to safety. The riskier, upper parts of the inverted pyramid become less liquid (harder to sell), and – if they can be sold at all – change hands at markedly lower prices as the once continuous flow of credit that had levitated those prices dries up.” In short, what Lewis Johnson outlines is the bottom-line rationale for diversifying one’s portfolio with gold.

U.S. gold bar and coin demand up 38% over last year

Map courtesy of the World Gold Council

The World Gold Council reports U.S. bar and coin demand rose 38% over the past year (through the first quarter). Global central banks and financial institutions drove physical gold demand the past 12 months raising once again the question if professional investors know something that retail investors do not. As the map above illustrates, the United States ranked at the top globally for growth in gold coin and bullion demand over the past year, while Asian demand fell back. Most of the U.S. demand, as previously mentioned, originated with funds and institutions, not individual private investors.

Here’s the World Gold Council’s summary of demand trends through the first quarter of 2019:

“Central banks bought 145.5t of gold, the largest Q1 increase in global reserves since 2013. Diversification and a desire for safe, liquid assets were the main drivers of buying here. On a rolling four-quarter basis, gold buying reached a record high for our data series of 715.7t. Q1 jewellery demand up 1%, boosted by India. A lower rupee gold price in late February/early March coincided with the traditional gold-buying wedding season, lifting jewellery demand in India to 125.4t (+5% y-o-y) – the highest Q1 since 2015. ETFs and similar products added 40.3t in Q1. Funds listed in the US and Europe benefitted from inflows, although the former were relatively erratic, while the latter were underpinned by continued geopolitical instability. Bar and coin investment softened a touch – 1% down to 257.8t. China and Japan were the main contributors to the decline. Japan saw net disinvestment, driven by profit-taking as the local price surged in February.”

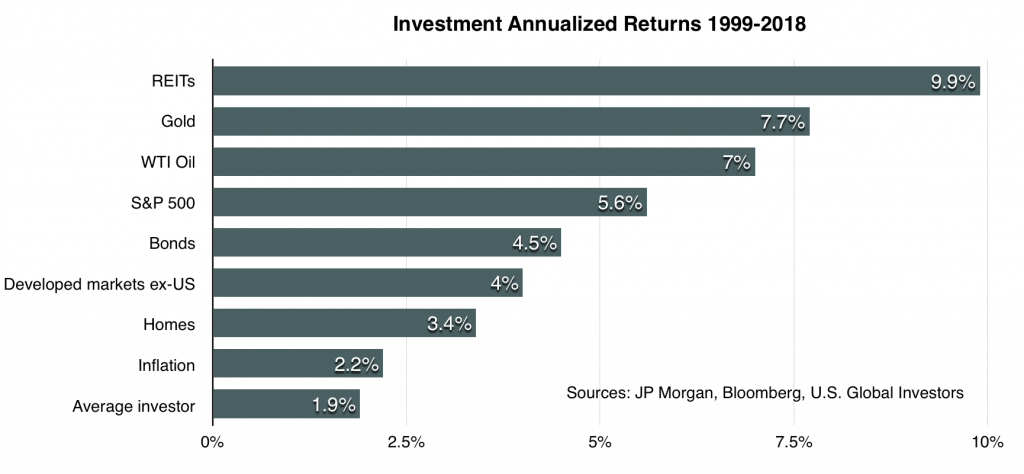

JP Morgan study ranks gold second best

investment over the past twenty years

J.P. Morgan Asset Management released a report recently ranking investments over the past twenty years. It shows gold as the second best performer over the period at a 7.7% average gain annually. REITs (Real Estate Investment Trusts) were number one at a 9.9% gain. Stocks ranked fourth at 5.6%.

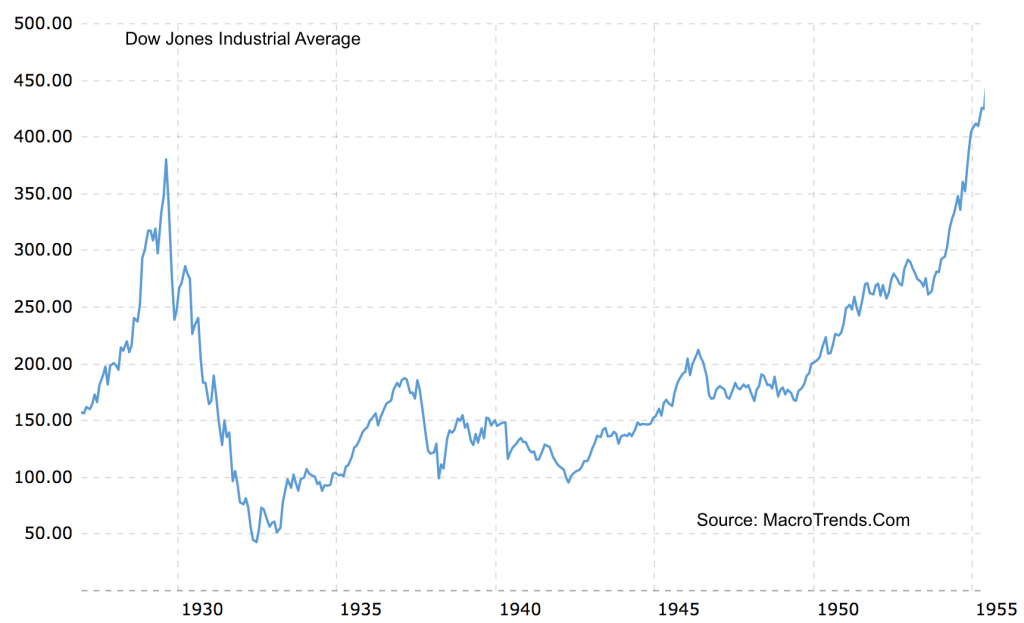

Why a 60%-65% stock market loss would be run-of-the-mill

Though the presence of bearish sentiment on stocks is widely acknowledged, it is also generally ignored. Too many believe that even if the stock market tumbles, it will quickly recover as it did after the 2007-2008 credit debacle. There is another scenario – the 1929 example – where the market does not return to peak values for decades (See chart below). “One might view the very comparison of present stock market conditions to 1929 market peak as exaggerated and preposterous, but then, one would be wrong,” says John Hussman of Hussman Funds, “The fact is that on the valuation measures we find most strongly correlated with actual subsequent long-term and full-cycle market returns across history (and even in recent decades), current market valuations match or exceed those observed at the 1929 peak.”

Chart courtesy of MacroTrends.com

Why the U.S. needs to encourage Americans to hold gold

We have always believed that citizen ownership of physical gold is in the national best interest, not just the best interest of its accumulators. In the event of a worldwide economic breakdown or a realignment of the global monetary system, it would be good for the country to have a storehouse of gold held by the populace. China encourages citizen gold ownership for precisely that reason.

“With a growing number of countries encouraging their central banks and citizens to acquire gold,” writes The Federalist‘s Sean Fieler, “it is increasingly reasonable to assume that gold will be part of the world’s monetary future, not just its past. The U.S. Treasury should embrace policies that will attract more of the world’s gold to America and better position our citizens and our nation for whatever the monetary future may hold.”

German citizens own a staggering 8918 tonnes of gold

Along these lines, Bullion Star‘s Ronan Manly published a stunning revelation that the German people have accumulated a “staggering” hoard of gold – 8918 tonnes – a hoard larger than that held by the United States government. The German central bank owns another 3370 tonnes, the second largest official sector holding after the United States.

In reading Manly’s analysis, we were reminded of the old aphorism – Those own the gold make the rules. “While the Chinese and Indian populations are well known for their insatiable appetite for importing, buying and hoarding physical gold,” he says, “there is one market in the West that does likewise but which flies under the radar slightly, garnering less attention than China and India. That gold market is Germany. Although German citizens are known for their fondness for holding gold, the vast size of the German population’s gold holdings was clarified recently in a newly published survey commissioned by Reisebank, a bank active in the German precious metals market.”

American Eagle bullion coin sales up sharply over last year

The U.S. Mint reports sales of American Eagle gold and silver bullion coins running well ahead of last year’s pace at the end of April. Gold Eagle sales were up 49.6% over the first four months of last year. Silver Eagle sales were up 35.2% over the same period. Month over month, Gold Eagle sales were nearly double the sales from April of last year. Silver Eagle sales were up 31% over March of last year. Many analysts consider bullion coin sales a bellwether for overall interest in the precious metals among investors. This year’s strong uptick over last year indicates increased activity among American investors interested in including gold and silver in their holdings as safe-haven hedges and an underpriced asset class.

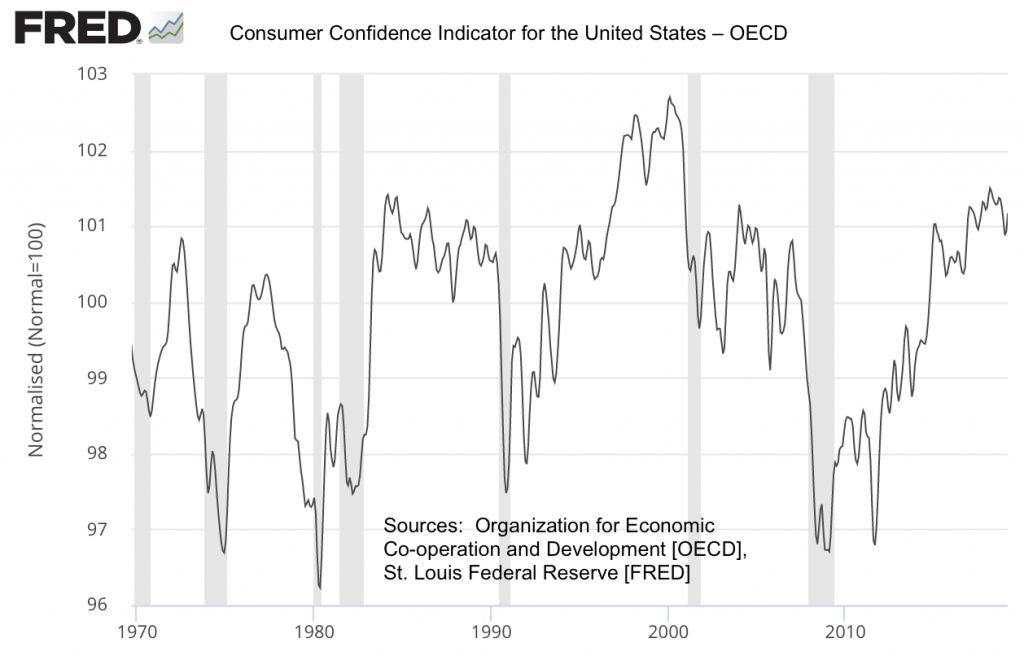

OECD indicator flashing danger ahead

The Organization for Economic Co-operation and Development (OECD) measures consumer confidence in various economies including the United States. A reading above 100 indicates a positive outlook toward the future economic situation. Values below 100 reflect a more pessimistic outlook. As you can see, we are now at a level in consumer confidence that has signaled downturns in the past. In fact, consumer confidence is now ahead of where it was just before the 2008-2009 recession and just below the level it registered before the dot.com stock market bust in 2000.

Why gold could rise for the next ten years

Bert Dohmen, editor of the Wellington Letter, called the twenty-year bear market in gold that began in 1981 and ended in 2001. Now in Forbes article, he reminds us not only of that call but the one that went with it. “The second part of our forecast in 1981 said that according to our very long-term cycle study, that bear market would be followed by a 30-year rise in gold. We even said we had no idea what would cause it, but the cycles said it should happen. If the forecast I made in 1981 still holds true, gold could have a continued secular bull market until 2030. That means the gold bull market could have about 11 more years to go. Historically, the final phase of a bull market is the most spectacular.” [Emphasis added]

The lesson is one as old as the gold market itself: The best time to buy is when the market is quiet – a strategy that requires both discipline and conviction. As an old friend and client of USAGOLD used to say (he passed away years ago): “It is not a question of if, but when.” He accumulated a large hoard of the metal in the 1990s and early 2000s between $300 and $600 per ounce and lived to see his prediction come true. His estate though was the ultimate beneficiary of his wisdom. He was not one to sell gold once he had acquired it. We chatted regularly on the phone back then and I told him that I had used the story just told in one of my newsletters. He was in his late 80s at the time. “Tell them,” he said resolutely, “that I bought my first ounce of gold at $35.”

A word on USAGOLD – USAGOLD ranks among the most reputable gold companies in the United States. Founded in the 1970s and still family-owned, it is one of the oldest and most respected names in the gold industry. USAGOLD has always attracted a certain type of investor – one looking for a high degree of reliability and market insight coupled with a professional client (rather than customer) approach to precious metals ownership. We are large enough to provide the advantages of scale, but not so large that we do not have time for you. (We invite your visit to the Better Business Bureau website to review our five-star, zero-complaint record. The report includes a large number of verified customer reviews.)

ORDER DESK

1-800-869-5115 Ext#100

[email protected]

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares is the founder of USAGOLD and the author of The ABCs of Gold Investing – How to Protect and Build Your Wealth With Gold [Third Edition]. He is also editor and commentator for USAGOLD’s Live Daily Newsletter and editor of the News & Views monthly newsletter.